A hard inquiry can drop your credit score anywhere from 0 to 21 points depending on your profile. They stay on reports for two years, stop impacting scores after 12 months, and often weigh heavier on younger credit files.

Hard Inquiries and the Real Impact They Have on Your Credit Score

Hard inquiries happen when a lender checks your credit during an application for a loan, credit card, or rental.

While many assume they only cost five points, the reality is more complicated.

The impact varies widely, from no drop at all to a sudden 20-point decline, depending on your credit history and the scoring model being used. Here’s what you need to know at a glance:

- Range of impact: 0 to 21 points depending on profile strength.

- Younger files: Hit harder than seasoned credit histories.

- Mortgage scoring: Older models penalize inquiries more.

- Duration: Remain on your report for 24 months, but only affect scores for 12.

- Caps: Around 14 inquiries, further ones may not lower scores but still raise lender concerns.

- Perception: Too many pulls can signal desperation, even if finances are solid.

Understanding how inquiries work helps you protect your score from unnecessary damage and gives you a clearer picture of what really matters to lenders.

But knowing the numbers is only the start.

To fully protect your credit, it’s essential to understand which inquiries can be removed, how to avoid unnecessary ones, and what lenders really look for behind the score.

Why Your Credit Score Needs to Stay Clean

Your credit score is more than a number. It is the reputation you carry into every financial decision, from getting a mortgage to leasing an apartment.

A strong score earns you approvals and better rates, while a weakened score can cost you thousands over time.

Why Inquiries Matter Even if They Seem Small

Inquiries make up only about 10 percent of your FICO score, yet their influence stretches further than that number suggests.

Lenders interpret them as signs of your borrowing habits, and too many can raise concerns even if your score is otherwise strong.

Hard vs Soft Inquiries Explained

Hard inquiries occur when you apply for new credit like a loan, credit card, or rental. These are recorded on your report and can reduce your score.

Soft inquiries happen when you check your credit or get pre-approved offers. They appear on your report but do not impact your score.

When Inquiries Look Like Red Flags

A series of hard pulls in a short period can make you look desperate for credit.

Even if your finances are in order, lenders may hesitate when they see multiple recent applications, interpreting them as higher risk.

The Myth of the “Five Point Drop”

Many blogs suggest a hard inquiry only costs five points. The reality is more complex.

Depending on your profile, the drop could be close to zero or as steep as 20 points. This gap between the myth and reality is where many borrowers are caught off guard.

Keeping your score clean starts with knowing that not all inquiries are harmless.

The next step is understanding exactly how much damage they can do and why the impact varies from person to person.

The Real Impact of Hard Inquiries on Your Credit Score

Most people believe that a hard inquiry only lowers a score by about five points.

While that’s often repeated, it’s misleading.

The actual impact depends heavily on your credit history, the scoring model in use, and how many recent applications you already have.

Point Range of Hard Inquiries

A hard inquiry can have no visible effect for some borrowers, while others may see a drop of up to 21 points.

The difference comes from how scoring systems group borrowers into categories, meaning the same inquiry can hit one person much harder than another.

Younger Credit Files

Borrowers with thin or young credit histories usually feel the impact more strongly.

A single inquiry might take away 10 to 20 points, while someone with a long track record and diverse accounts might only lose a couple points.

Mortgage Scoring Models

Older mortgage scoring versions such as FICO 2, 4, and 5 are tougher on inquiries compared to FICO 8 or 9.

This is why inquiries can weigh more heavily when someone applies for a home loan compared to other forms of credit.

How Inquiries Age

Hard inquiries stay on a report for two years, but they stop affecting the score after 12 months. The recovery is not gradual.

The points return all at once when the one-year mark is reached.

Penalty Caps in Scoring

Some FICO models include a maximum penalty cap.

Once a borrower has about 14 inquiries, additional ones usually do not lower the score further. Lenders, however, can still view a long list of inquiries as a warning sign.

Hard inquiries are not a flat five-point penalty.

They can range widely depending on the circumstances, and even when points return, the perception of risk can linger.

This brings us to the next question borrowers often ask: when can these inquiries actually be removed, and when must they remain?

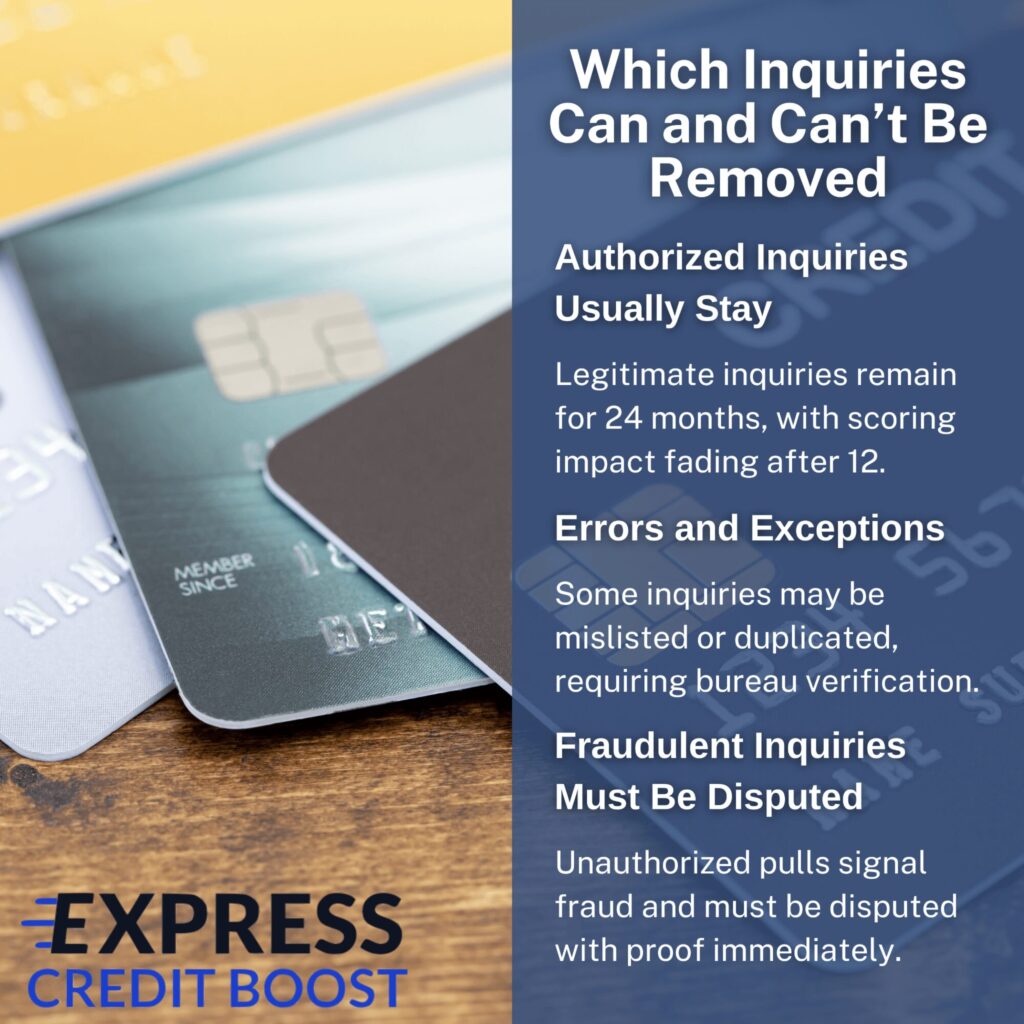

When Hard Inquiries Can Be Removed and When They Can’t

Not all inquiries on your credit report are created equal, and not all of them can be erased.

Understanding the difference between legitimate and unauthorized pulls is the first step toward knowing what action is possible.

Legitimate vs Unauthorized Inquiries

A legitimate inquiry occurs when you apply for credit and authorize the lender to review your report. These cannot be disputed or removed simply because they lowered your score.

Unauthorized inquiries, however, are another story.

If your credit is pulled without your permission, or as the result of identity theft, you have the right to dispute them with the bureaus.

The Misconception About Total Removal

A common misunderstanding in credit repair is that all inquiries can be erased.

This is not the case.

Only errors, duplicates, or fraudulent inquiries can be legally challenged. Any company promising to wipe away every inquiry is not being transparent about the rules.

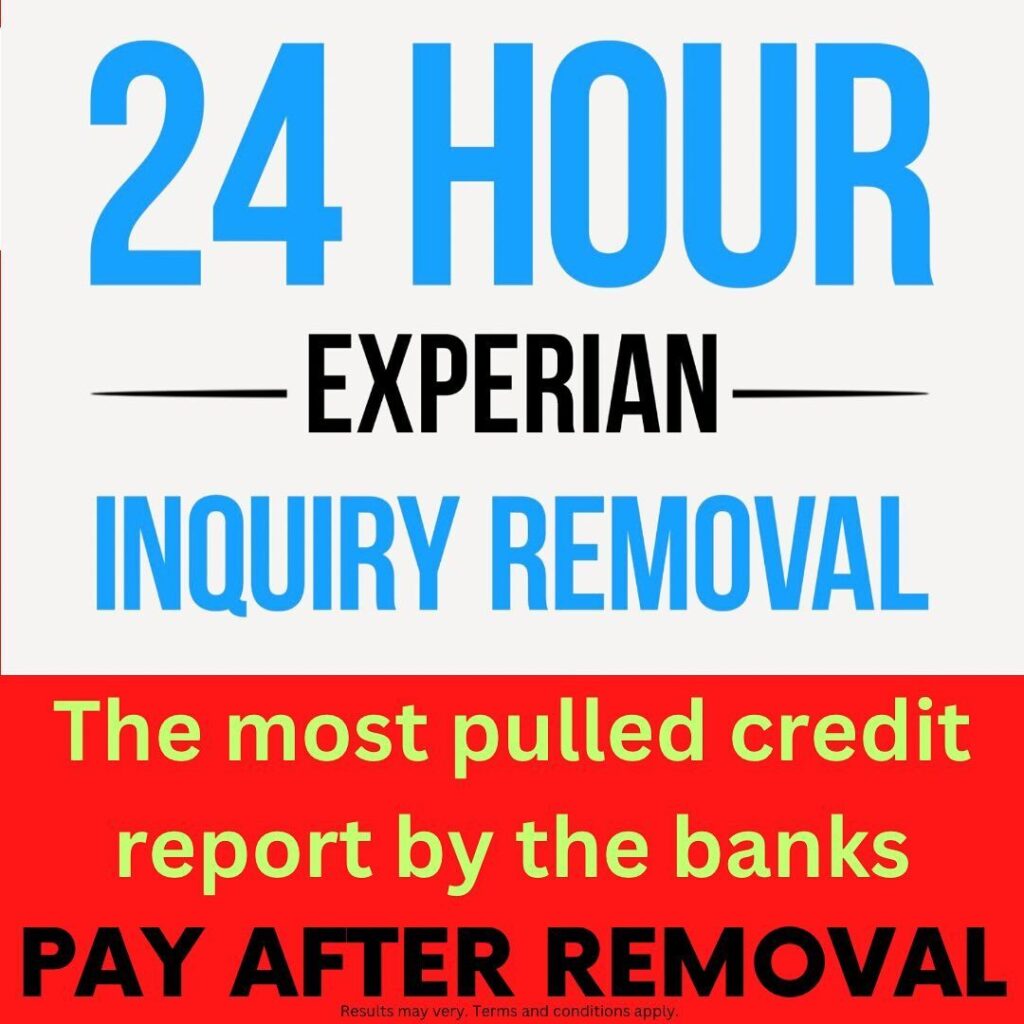

Professional Tools for Faster Results

While inquiries tied to legitimate accounts must stay, there are ways to contest those that do not belong. Some services specialize in fast resolutions.

For example, certain firms have refined the process of working directly with Experian, allowing for same-day removal in some cases.

This is particularly valuable for people pursuing SBA loans or business financing, where Experian inquiries carry significant weight.

One documented case even involved the successful removal of 80 inquiries at once.

DIY vs Professional Help

Disputing inquiries yourself is possible, but it comes with heavy paperwork.

Typical filings can run 10 to 20 pages, require legal citations, and demand repeated follow-up with the bureaus.

Add in the costs of certified mail and the process quickly becomes time-consuming and expensive.

Professional services have teams and systems in place to handle these disputes efficiently, often at a scale that individuals simply cannot replicate.

Knowing what can and cannot be removed saves borrowers from frustration and wasted effort.

Once you understand these limits, the next step is learning how to avoid unnecessary inquiries before they ever show up on your report.

How to Protect Your Credit from Hard Inquiries in the First Place

The easiest way to deal with hard inquiries is to avoid unnecessary ones before they appear on your report.

With a few smart habits, you can limit the damage and keep your credit profile strong.

Use Pre-Qualification Tools

Many lenders and credit card issuers now offer pre-qualification or pre-approval options that only trigger a soft pull.

These allow you to check your odds of approval without sacrificing points on your credit score.

Apply Strategically, Not Frequently

Spacing out applications helps you avoid clusters of inquiries that may look like financial distress.

Only apply for new credit when it is truly necessary, and avoid multiple applications within short time frames.

Be Cautious at Auto Dealerships

Car dealers often submit applications to several lenders at once.

While FICO may group these into a single inquiry, not every scoring model does. If you are financing a car, ask the dealer before they run your credit and limit the number of lenders they contact.

Manage Credit Freezes Wisely

If you have a credit freeze in place, lift it only when you intend to apply. This prevents unauthorized pulls and reduces the risk of identity theft.

Monitor Your Reports Regularly

Checking your credit reports helps you catch unauthorized inquiries early. Quick action can prevent fraudulent pulls from turning into bigger problems.

While hard inquiries are not permanent marks, preventing unnecessary ones is the best way to protect your score.

And even if inquiries bring a temporary dip, recovery is usually steady, especially if your overall profile remains strong.

Don’t Let Hard Inquiries Hold You Back

Hard inquiries may only account for a small share of your credit score, but their impact can reach far beyond the numbers.

A cluster of inquiries at the wrong time can tip the balance between approval and denial, especially when it comes to sensitive situations like securing a mortgage or qualifying for an SBA loan.

Lenders often read multiple inquiries as signs of desperation, which can affect decisions even if your score remains strong.

The key is knowing which inquiries truly matter, which can be removed, and how to prevent unnecessary ones from piling up in the first place.

By staying proactive, you safeguard not just your score but also your financial reputation.

If you’re stuck with hard inquiries dragging down your score, talk to Express Credit Boost today. Our 24-hour Experian removal service can help you recover lost points and get approved again.